Highlights:

- Understanding the Credit Report

- Know the Credit Score Range and What it Implies

- Know How to Read a Credit Report

Your credit report or CIBIL report showcases your monetary health providing a deeper insight into the state of your overall finances. It forms an integral part of your credit score and helps lending institutions make financial decisions regarding extending loans and their terms. Once you understand what constitutes a credit report, reading its contents becomes much simpler.

What is a Credit Report?

A credit report is a detailed record of your credit history about loans and credit cards that you own and how responsibly you pay the respective EMIs and bills. Individuals can access their credit reports from any of the four credit bureaus in India – TransUnion CIBIL, CRIF High Mark, Equifax, and Experian. Each credit agency compiles credit information from various lending institutions in the form of a credit report. Thereafter, they assign a three-digit numeral, commonly known as a credit score. A credit score assigned by TransUnion CIBIL is known as a CIBIL score.

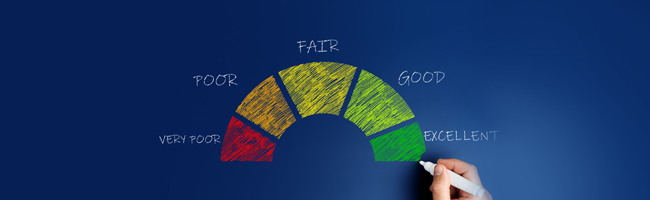

Credit Score Range

Here is a quick look at the different ranges of credit scores and what each of them implies while availing credit:

| Your CIBIL Score | What it implies |

|---|---|

| 800 - 900 | An excellent score range that suggests consistent payments without any defaults on EMIs and credit bills. |

| 750 - 800 | This is a very good CIBIL score and you are now in a position to negotiate for a better interest rate. |

| 625 – 750 | You have a decent credit history with very few irregularities. You may get a loan but at a higher interest rate. |

| 300 – 625 | This score indicates high frequencies of defaults and irregularities. You may find it very difficult to get a loan unless you improve your CIBIL score. |

Also Read: 7 Tips to Help You Improve Your CIBIL Score

How to Read a Credit Report?

A credit report comprises various sections with different categories of information. Each credit bureau has its own format but the general compilation of the sections is as follows:

1. Credit Score

A credit score is a numerical representation of your credit history ranging between 300 and 900. Lenders evaluate it before approving any credit to determine your eligibility and the appropriate terms.

2. Personal and Account Information

This section contains your personal and account information. It mentions details like types of loans, account numbers, ownership details, important dates, loan amount, and month-by-month data of your loan accounts up to the last three years. It also references your credit balance, available limit, account type, account status, and payment history.

3. DPD Information

DPD or ‘Days Past Dues’ is a record of your credit payment timelines. Even a delay of one day is reflected here either as a remark or a number. For example, if there is a delay of four days, it will be marked numerically. If you default by 0 days, it may be indicated with a numeral or a comment. ‘XXX’ means unreported information. A DPD other than ‘000’ or ‘XXX’ implies that one has not paid their dues regularly.

4. Enquiry Information

Enquiry information encompasses both hard and soft enquiries. A soft enquiry is the one made by you, businesses offering you goods or services and your existing creditor. It doesn’t affect your credit score unlike a hard enquiry, which is usually initiated by prospective lenders after they receive credit applications. A single hard enquiry may be harmless but too many credit requests can reduce your score.

5. Credit Report Remarks

The remarks section shows the current state of your accounts. Given below are some lender’s comments that one may commonly find in a credit report:

-

Settled

Partly paying the dues to settle a loan or credit card may attract a ‘settled’ remark. This has negative connotations for your credit score and future credit aspirations.

-

Written Off

The inability to pay off the outstanding loan/credit card amount for more than 180 days is reported as a ‘written off’ note and may hurt your credit score.

-

Post Write-Off Settled

A ‘post write-off settled’ comment denotes debt settlement after your credit has been written off. This can damage your credit health, denying you any credit in the future.

-

Wilful Default

A wilful default happens when borrowers do not repay the loan despite having the means to do so. Those who utilise loan funds for unfair purposes other than the reason for which they were originally availed are also brought under the purview of wilful default. Such borrowers are seriously dealt with, sometimes necessitating legal action.

-

Closed

When you pay off your loan in full, lenders report the account as ‘closed’. They also issue a ‘No Dues Certificate’ or closure letter stating the loan cleared.

It is imperative to read and fathom one’s credit reports for easier monitoring of the records and to maintain a healthy CIBIL score or even improve it, if necessary. Tracking your report periodically enables you to check its accuracy. In case of any discrepancies or mistakes, report them to the credit bureau immediately. They will consult the financial institution in question before effecting the necessary changes. Your credit records let you make more informed decisions regarding your spending habits and credit behaviour as a diligent borrower.

DISCLAIMER:

While care is taken to update the information, products, and services included in or available on our website and related platforms/websites, there may be inadvertent errors or delays in updating the information. The material contained in this website and on associated web pages, is for reference and general information purposes, and the details mentioned in the respective product/service document shall prevail in case of any inconsistency. Users should seek professional advice before acting on the basis of the information contained herein. Please take an informed decision with respect to any product or service after going through the relevant product/service document and applicable terms and conditions. Neither Bajaj Housing Finance Limited nor any of its agents/associates/affiliates shall be liable for any act or omission of the Users relying on the information contained on this website and on associated web pages. In case any inconsistencies are observed, please click on contact information.

Content with tag .

Trending Articles

cibil Cibil

[N][T][T][N][T]

Boost Your Credit Score By Minding The Factors That Affect It2023-03-20 | 5 min

cibil Cibil

[N][T][T][N][T]

How to Check Your CIBIL Score for Free and What to Do If There Are Errors in It2024-06-05 | 4 min

cibil Cibil

[N][T][T][N][T]

Check CIBIL Score with PAN Card for Free, in 3 Steps2024-02-27 | 5 min

cibil Cibil

[N][T][T][N][T]

CIBIL Score Charges & Services You Must Know2023-04-04 | 2 min

cibil Cibil

[N][T][T][N][T]

What to Know About CIBIL Score 2.02024-06-20 | 3 min

cibil Cibil

[N][T][T][N][T]

Some of the Common Credit Mistakes to Avoid2023-03-21 | 4 min

cibil Cibil

[N][T][T][N][T]

Will a Loan Settlement Ruin My CIBIL Score?2023-03-21 | 4 min

cibil Cibil

[N][T][T][N][T]

How can I Remove Loan Inquiry from CIBIL Credit Report2024-01-22 | 5 min

cibil Cibil

[N][T][T][N][T]

How To Improve CIBIL Score After A Payment Default?2024-03-29 | 4 min

cibil Cibil

[N][T][T][N][T]

Here Is How a Bounced Cheque Can Affect Your CIBIL Score2023-06-06 | 5 min

cibil Cibil

[N][T][T][N][T]

How to Increase Your CIBIL Score Above 800: 6 Proven Methods2024-01-24 | 4 min

cibil Cibil

[N][T][T][N][T]

Does Applying for Credit Affects One's CIBIL Score?2024-03-14 | 3 min

cibil Cibil

[N][T][T][N][T]

10 Effective Strategies for Boosting Your Credit Rating2023-03-24 | 6 min

cibil Cibil

[N][T][T][N][T]

How Does Being A Loan Guarantor Affect Your Credit Score?2024-03-13 | 4 min

cibil Cibil

[N][T][T][N][T]

What's Considered a Healthy Credit Mix?2024-06-11 | 3 min

cibil Cibil

[N][T][T][N][T]

What Distinguishes CIBIL Score from CIBIL Report?2024-04-11 | 3 min

cibil Cibil

[N][T][T][N][T]

What is Credit Mix and How to Boost Your Credit Score?2023-03-27 | 7 min

cibil Cibil

[N][T][T][N][T]

Does CIBIL Score Affect Loan Against Property Eligibility?2023-02-15 | 7 min

cibil Cibil

[N][T][T][N][T]

What Is a Good Credit Score for a Home Loan?2022-12-28 | 5 min

cibil Cibil

[N][T][T][N][T]

Things That Can Go Wrong with Your CIBIL Report2023-03-15 | 5 min

cibil Cibil

[N][T][T][N][T]

How a Good CIBIL Score Can Help You Celebrate the Festive Season Better2024-03-19 | 5 min

cibil Cibil

[N][T][T][N][T]

How Can Your CIBIL Score Help in Negotiating Better Home Loan Deals2023-05-18 | 4 min

cibil Cibil

[N][T][T][N][T]

Here’s What You Can Do to Improve Your CIBIL Score2023-03-16 | 4 min

cibil Cibil

[N][T][T][N][T]

Top 10 Reasons For Low CIBIL Score & How To Improve It2024-03-01 | 5 min

cibil Cibil

[N][T][T][N][T]

Five Reasons Why a Bad Credit Score Could Lead to Loan Rejection2024-01-22 | 5 min

cibil Cibil

[N][T][T][N][T]

How Does Your Digital Footprint Affect Your CIBIL Score?2024-03-20 | 5 min

cibil Cibil

[N][T][T][N][T]

How Can I Get My ECN Number in CIBIL?2024-01-09 | 5 min

cibil Cibil

[N][T][T][N][T]

Ways You Can Improve your Credit Score for a Small Business2023-03-01 | 5 min

cibil Cibil

[N][T][T][N][T]

Reasons Why Your CIBIL Score Is Going Down2024-04-10 | 4 min

cibil Cibil

[N][T][T][N][T]

How Business Loans Affect Your CIBIL Score & How to Improve the Same2024-03-13 | 6 min

cibil Cibil

[N][T][T][N][T]

How Does Missing One Payment Affect Your CIBIL Score?2024-05-15 | 4 min

cibil Cibil

[N][T][T][N][T]

Ways to Improve Your Credit Score with a Credit Card2024-02-02 | 4 min

cibil Cibil

[N][T][T][N][T]

What Factors Do Not Affect Credit Scores?2024-02-28 | 7 min

cibil Cibil

[N][T][T][N][T]

How to Check, Calculate, and Improve CIBIL Score?2024-01-11 | 2 min

cibil Cibil

[N][T][T][N][T]

Easy Ways to Maintain a Good Business Credit Score2024-01-10 | 5 min

cibil Cibil

[N][T][T][N][T]

Impact of Late Payment on CIBIL Score?2024-03-08 | 6 min

cibil Cibil

[N][T][T][N][T]

Pay Minimum Amount Due on Your Credit Cards Will Impact Your Credit Score2024-03-11 | 5 min

cibil Cibil

[N][T][T][N][T]

Here’s How a Short-term Loan Can Help You Improve Your CIBIL Score2024-03-25 | 5 min

cibil Cibil

[N][T][T][N][T]

How Can I Raise My Credit Score From 360 to 800 Within a Year?2024-03-21 | 5 min

cibil Cibil

[N][T][T][N][T]

Does a Name Change Affect Your Credit Score2024-01-07 | 4 min

cibil Cibil

[N][T][T][N][T]

Everything You Should Know About Your CIBIL Score2024-02-09 | 7 min

cibil Cibil

[N][T][T][N][T]

What is Credit Score and Its Impact on Loan Availability2023-03-27 |

cibil Cibil

[N][T][T][N][T]

What Does Your Credit Score Tell About You?2024-06-11 | 5 min

cibil Cibil

[N][T][T][N][T]

Know How Mortgage Loan Affect Your CIBIL Score2024-02-05 | 5 Min

cibil Cibil

[N][T][T][N][T]

Why is a CIBIL Score Measured Between 300 and 900?2024-05-07 | 4 min

cibil Cibil

[N][T][T][N][T]

What are the Types CIBIL Errors & How to Correct Them?2023-11-22 | 6 min

cibil Cibil

[N][T][T][N][T]

What is CIBIL? Understand How It Works and Its Importance2024-01-31 | 6 min

cibil Cibil

[N][T][T][N][T]

What Are Tradelines and How to Find Them On Your Credit Report?2024-05-28 | 4 min

cibil Cibil

[N][T][T][N][T]

Introduction to Credit Information Bureau India Limited (CIBIL)2024-04-15 | 6 min

cibil Cibil

[N][T][T][N][T]

What Does a Zero or Negative Credit Score Mean?2023-02-24 | 4 min

cibil Cibil

[N][T][T][N][T]

How Many Credit Inquiries are Too Much in a Year2023-09-21 | 2 min

cibil Cibil

[N][T][T][N][T]

How to Check CIBIL Score Online?2023-03-14 | 5 min

cibil Cibil

[N][T][T][N][T]

10 Common Myths About CIBIL Score2024-03-27 | 4 min

cibil Cibil

[N][T][T][N][T]

Difference Between Credit Score and CIBIL Score2024-02-15 | 5 min

cibil Cibil

[N][T][T][N][T]

Loan Settlement And Its Effects On Your Credit Score2024-03-07 | 6 min

cibil Cibil

[N][T][T][N][T]

Everything You Need to Know About the Ideal CIBIL Score for Business Loan2024-01-17 | 4 min

cibil Cibil

[N][T][T][N][T]

What is the Role of CIBIL Score in Getting a Home Loan?2024-05-08 | 5 min

cibil Cibil

[N][T][T][N][T]

Impact Of a Co-Applicant’s CIBIL Score On Your Home Loan Application2023-01-20 | 4 min

cibil Cibil

[N][T][T][N][T]

How is CIBIL Score Calculated - Factors That Affect CIBIL Score Calculations2023-03-22 | 6 min

cibil Cibil

[N][T][T][N][T]

What Is Credit Utilization Ratio and How Can You Improve It?2023-03-23 | 5 min

cibil Cibil

[N][T][T][N][T]

Different Types of Credit Report Errors and How to Fix Them_WC2023-07-11 | 4 min

cibil Cibil

[N][T][T][N][T]

What Is Credit Mix and How Can It Help Your Credit Score?2023-07-12 | 3 min

cibil Cibil

[N][T][T][N][T]

How to Get a Good Credit Mix and Boost Your Credit Score2023-07-11 | 4 min

cibil Cibil

[N][T][T][N][T]

Why Is CIBIL Score Important for Your Financial Health?2023-04-17 | 3 min

cibil Cibil

[N][T][T][N][T]

What is CIBIL Score and How is it Impacted by a Missed EMI?2023-05-31 | 2 min

cibil Cibil

[N][T][T][N][T]

The Role of CIBIL Score in Determining your Home Loan Disbursement Amount2023-05-31 | 2 min

cibil Cibil

[N][T][T][N][T]

Minimum CIBIL Score for Business Loans2023-04-17 | 5 min

cibil Cibil

[N][T][T][N][T]

Tips to Maintain Your Business CIBIL Score Above 7002023-02-02 | 5 min

cibil Cibil

[N][T][T][N][T]

Is a Good CIBIL Score Mandatory for Home Loan Approval?2023-02-17 | 4 min

cibil Cibil

[N][T][T][N][T]

Importance of CIBIL Score & Tips To Improve It2023-02-21 | 5 min

cibil Cibil

[N][T][T][N][T]

What is the Procedure to Check your CIBIL Score Rating?2023-03-27 | 4 min

cibil Cibil

[N][T][T][N][T]

Different Types of Credit Scoring Models You Must Know2023-03-16 | 5 min

cibil Cibil

[N][T][T][N][T]

How Do You Establish a Credit Score for the First Time?2023-03-22 | 6 min

cibil Cibil

[N][T][T][N][T]

Ways to Maintain a Healthy Credit Score and Profile2023-03-13 | 6 min

cibil Cibil

[N][T][T][N][T]

Top Tips to Improve Credit Score Immediately to Get Your Loan Approved2023-03-30 | 5 min

cibil Cibil

[N][T][T][N][T]

Reasons to Maintain a Positive Credit Profile and a High CIBIL Score2023-03-01 | 5 min

cibil Cibil

[N][T][T][N][T]

Importance of CIBIL Score for Achieving Business Goals2023-03-16 | 5 min

cibil Cibil

[N][T][T][N][T]

What Does Your Credit Score Reveal About You?2023-04-05 | 5 min

cibil Cibil

[N][T][T][N][T]

7 Tips to Help You Improve Your CIBIL Score2022-12-21 | 5 min

cibil Cibil

[N][T][T][N][T]

Why Is It Important to Check Your Credit Report and How Often?2023-03-22 | 3 min

cibil Cibil

[N][T][T][N][T]

Why is Credit Score Important After Retirement?2023-03-22 | 6 min

cibil Cibil

[N][T][T][N][T]

5 Ways to Increase CIBIL Score After Job Loss2023-03-21 | 4 min

cibil Cibil

[N][T][T][N][T]

Here’s What These Various Sections of a CIBIL Report Mean2023-03-21 | 5 min

cibil Cibil

[N][T][T][N][T]

7 Easy Tips On How Chartered Accountants Can Increase Their CIBIL Score?2023-01-23 | 4 min

cibil Cibil

[N][T][T][N][T]

High CIBIL Score Helps Low-Interest Rate Loans2023-09-20 | 5 min

cibil Cibil

[N][T][T][N][T]

How Long Does It Take to Improve a CIBIL Score2023-03-29 | 5 min

cibil Cibil

[N][T][T][N][T]

How Can Customers Check Their Credit History?